Event aims to boost flagging market by offering buyers and investors a one-stop shop of new condo projects

Presale buyers at the Soleil White Rock condo project can earn eight per cent interest on their deposit during the three years it will take to finish the 178-unit luxury tower | Submitted

B.C.’s real estate and development industry has been full of innovative ways to sell new condos recently, and now it is taking another fresh approach to sales with Canada’s first ever CondoExpo.

The event, to be held at the JW Marriott Parq Hotel in downtown Vancouver on Saturday September 28, will offer homebuyers and investors a one-stop shop for purchasing a new home.

The expo has been created by “real estate and development industry leaders” and will bring together many development companies from Metro Vancouver and further afield who are promoting their new residential projects.

Aly Armstrong, event director, said in a media statement, “CondoExpo will surely be the most state-of-the-art and experiential condo shopping experience Vancouverites have ever seen. Never before have the city’s top projects and developers come together to harmoniously allow buyers to be educated and empowered in their purchase decision in such a luxurious setting.”

A media release issued by Armstrong said, “Attendees will be empowered by unprecedented options and information from developers and breakout sessions hosted by industry leaders. CondoExpo will surely set a new standard for shopping in a city where real estate tends to be one of the hottest topics.”

Armstrong told Glacier Media, “CondoExpo will host its inaugural event in Hong Kong in August (next month). This will be the first expo of its kind in Canada and Vancouver will be our first stop in North America. CondoExpo has plans to expand across Canada and into the U.S.

“I can confirm we are working with some of the top developers, real estate marketing agencies and realtors in Vancouver. Buyers can expect to see a variety of the best condo projects available in Vancouver. We also will have projects around the province: Vancouver Island, Langley, Maple Ridge and Peachland to name a few.”

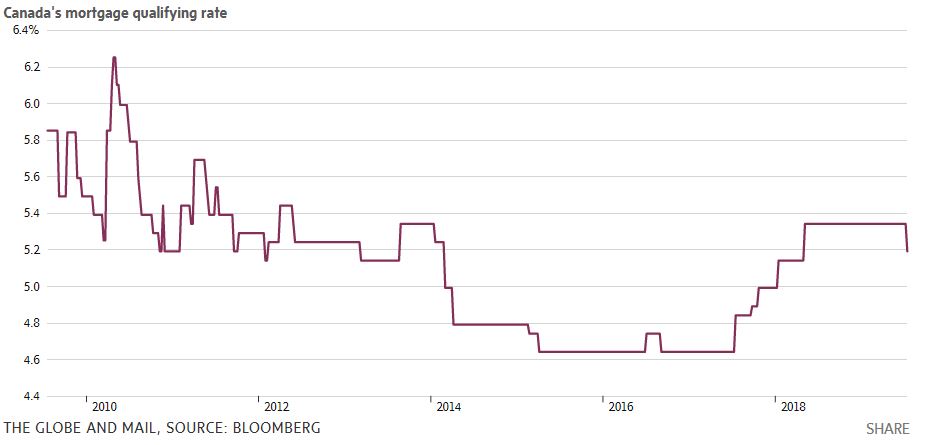

Qualifying Mortgage Rate Falls For First Time Since B-20 Intro

The interest rate used by the federally regulated banks in mortgage stress tests has declined for the first time since 2016, making it a bit easier to get a mortgage. This is particularly important for first-time homeowners who have been struggling to pass the B-20 stress test. The benchmark posted 5-year fixed rate has fallen from 5.34% to 5.19%. It’s the first change since May 9, 2018. And it’s the first decrease since Sept. 7, 2016, despite a 106-basis-point nosedive in Canada’s 5-year bond rate since November 8 (see chart below).

Five-Year Canadian Bond Yield

The benchmark qualifying mortgage rate is announced each week by the banks and “posted” by the Bank of Canada every Thursday as the “conventional 5-year mortgage rate.” The Bank of Canada surveys the six major banks’ posted 5-year fixed rates every Wednesday and uses a mode average of those rates to set the official benchmark. Over the past 18-months, since the revised B-20 stress test was implemented, posted rates have been almost 200 basis points above the rates banks are willing to offer, and the banks expect the borrower to negotiate the interest rate down. Less savvy homebuyers can find themselves paying mortgages rates well above the rates more experienced homebuyers do. Mortgage brokers do not use posted rates, instead offering the best rates from the start.

The benchmark rate (also known as, stress test rate or “mortgage qualifying rate”) is what federally regulated lenders use to calculate borrowers’ theoretical mortgage payments. A mortgage applicant must then prove they can afford such a payment. In other words, prove that amount doesn’t cause them to exceed the lender’s standard debt-ratio limits.

The rate is purposely inflated to ensure people can afford higher rates in the future.

The impact of the B-20 stress test has been very significant and continues to be felt in all corners of the housing market. As expected, the new mortgage rules distorted sales activity both before and after implementation. According to TD Bank economists in a recent report, “The B-20 has lowered Canadian home sales by about 40k between 2017Q4 and 2018Q4, with disproportionate impacts on the overvalued Toronto and Vancouver markets and first-time homebuyers…All else equal, if the B-20 regulation was removed immediately, home sales and prices could be 8% and 6% higher, respectively, by the end of 2020, compared to current projections.”

According to Rate Spy, for a borrower buying a home with 5% down, today’s drop in the stress-test rate means:

Someone making $50,000 a year can afford $2,800 (1.3%) more home

Someone making $100,000 a year can afford $5,900 (1.3%) more home

(Assumes no other debts and a 25-year amortization. Figures are rounded and approximate.)

For a borrower buying a home with 20% down, today’s drop in the stress-test rate means:

Someone making $50,000 a year can afford $4,000 (1.4%) more home

Someone making $100,000 a year can afford $8,300 (1.4%) more home

(Assumes no other debts and a 30-year amortization. Figures are rounded and approximate.)

Bottom Line: Almost no one saw this coming due to the stress test rate’s obscure and arcane calculation method (see Note below). This 15 basis point drop in in the qualifying rate will not turn the housing market around in the hardest-hit regions, but it will be an incremental positive psychological boost for buyers. It should also counter, in some small part, what’s been the slowest lending growth in five years.

Note: Here’s the scoop on why the qualifying rate fell. According to the Bank of Canada:

“There are currently two modes at equal distance from the simple 6-bank average. Therefore, the Bank would use its assets booked in CAD to determine the mode. We use the latest M4 return data released on OSFI’s website to do so. To obtain the value of assets booked in CAD, simply do the subtraction of total assets in foreign currency from total assets in total currency.”

The BoC explains further:

“Prior to July 15th, we were using April’s asset data to determine the typical rate as that was what was published on OSFI’s website. On July 15th, OSFI published the asset data for May, and that is what we used yesterday to determine the 5-year mortgage rate. As a result, the rate changed from 5.34% to 5.19%.”

Bank of Canada cuts mortgage stress test rate for first time since 2016

Canadians may now be able to afford slightly more expensive homes

For the first time in almost three years, the Bank of Canada has cut its minimum mortgage qualifying rate, dropping it to 5.19 per cent from 5.34 per cent.

The central bank’s new rate has a slight effect on the mortgage stress test for those with uninsured mortgages.

“At a minimum, the qualifying rate for all uninsured mortgages should be the greater of the contractual mortgage rate plus two per cent or the five-year benchmark rate published by the Bank of Canada,” states OSFI’s Residential Mortgage Underwriting Practices and Procedures guideline.

Whichever rate is higher is the one that borrowers are tested at. As a result, at least for the time being, it will be slightly easier for those with uninsured mortgages to qualify. This also applies to those who want to switch lenders.

According to calculations by RateSpy.com, assuming no other debts and a 30-year amortization period, someone earning $50,000 a year and making a 20 per cent down payment would be able to afford a home that is roughly $4,000 more expensive. Someone earning $100,000 a year and making the same down payment would be able to afford a home that is roughly $8,300 more expensive.

“This decrease alleviates some of the pressure on first-time homebuyers, who are the most financially strained Canadians entering the housing market,” said James Laird, co-founder of RateHub Inc. and president of CanWise Financial.

The Bank of Canada determines the conventional five-year mortgage rate using Office of the Superintendent of Financial Institutions (OSFI) data on the posted five-year rates for the six largest banks. OSFI on July 15 released the May data.

Canadian housing enters a new ‘boring’ era amid modest gains in sales

The incremental gains mark a new period of stability for housing sales after a less-than-stellar 2018 and early 2019

New home sales in Canada edged up 0.3 per cent in June from the previous month, with gains in the Greater Toronto Area and Montreal offsetting declines in B.C. The incremental gains mark a new period of stability for housing sales after a less-than-stellar 2018 and early 2019, according to the Canadian Real Estate Association’s monthly report.

While seasonally adjusted sales actually fell 0.2 per cent, they remain slightly above year-ago levels.

“The big story here is that sales and prices are essentially flat on a national basis, the market is close to overall balance, and sales activity is almost right on top of its 10-year average,” said Douglas Porter, BMO chief economist. “In other words, the Canadian housing market is now actually kind of boring, which is likely exactly what policymakers would like to see.”

The national average sale price was up 1.7 per cent on a year-over-year basis, coming in at just under $505,500. This figure is heavily skewed by the GTA and GVA markets: removing them would cut the price by $106,000.

On a month-to-month basis, new listings rose by 0.8 per cent.

One thing that hasn’t changed is the increasing deviation between the eastern and western markets in the country.

“While sales activity in Canada’s three westernmost provinces appears to have stopped deteriorating, it will be some time before supply and demand there becomes better balanced and the outlook for home prices improves,” said Gregory Klump, CREA’s chief economist in a press release.

More than 80 per cent of all local markets were in balanced market territory in June, the largest share in three years. The inventory of unsold homes dipped to 5.0 months, the lowest in a year and a half.

“We judge that the overall national market is more likely to strengthen modestly over the next 18 months, and are looking for sales and prices to both rise roughly 2 per cent in 2020,” said Porter. “Maybe not a moonshot, but not a bleak landscape either.”

B.C. government says ride hailing services can operate starting Sept. 16

The provincial government says its regulations for ride hailing will be in effect as of Sept. 16, 2019. Seth Wenig / AP

Welcome to B.C., Uber and Lyft.

The ride hailing companies could be operating on B.C. roads as early as Sept. 16, as the provincial government announced Monday its regulations on licensing and insurance for ride hailing will be in effect as of that date.

However, ride hailing companies would first need to apply for permission to operate through the Passenger Transportation Board. Applications will be accepted beginning Sept. 3.

The PTB, an independent board, is also responsible for setting guidelines around supply, boundaries and fares.

“Our plan has made it possible for ride-hailing companies to apply to enter the market this fall, with vehicles on the road later this year, while ensuring the safety of passengers and promoting accessibility options in the industry,” said Transportation Minister Claire Trevena in a statement.

“British Columbians have been asking and waiting for these services after more than five years of delay by the former government. We took action to allow for the services people want and we’re delivering on that promise.”

The Passenger Transportation Act regulations will require criminal record checks and annual driver record checks for any driver working with a ride-hailing company, and will introduce a new 30-cent per-trip fee and a $5,000 annual licence fee for the company.

The Motor Vehicle Act regulations will change how frequently cars must undergo inspections, will remove seatbelt exceptions for all for-hire vehicles, and will introduce side-entry accessible taxis.

“Currently taxi drivers are exempt from wearing seatbelts when travelling less than 70 kilometres an hour. This is an outdated regulation from the 70s,” said Steven Haywood, the Ministry of Transportation’s executive lead for taxi modernization and ride hailing. “This means taxi drivers and ride hail drivers will always have to wear their seatbelts.”

Drivers working for ride hailing companies are still required to hold a Class 4 commercial licence, a requirement supported by B.C.’s police chiefs association, but that was not recommended by a legislative committee tasked with making recommendations for ride hailing.

A majority of the committee proposed that ride-hail drivers should be allowed to work with the more common Class 5 licence rather than a Class 4, which is a commercial licence held by taxi and limo drivers, but B.C.’s NDP government is insisting on the Class 4 requirement.

“The requirement is not negotiable for to us, safety is of utmost responsibility. And we believe that it is our responsibility as the government to ensure that any public consumer service like this is held to a standard that they can rely on and trust in,” Bowinn Ma, MLA for North Vancouver-Lonsdale, said during a media call Monday.

NDP MLA Bowinn Ma says the Class 4 requirement is non-negotiable.

Alberta, which has Uber, requires ride hailing drivers hold a Class 1, 2 or 4 licence, all of which are for professional drivers. Most other provinces do not require a commercial licence.

Aaron Zifkin, the managing director of Lyft Canada, says his company, which has cars in Toronto and Ottawa along with 640 U.S. cities, does not currently operate in any jurisdiction that requires drivers to have a commercial driver’s licence.

Commercial licences for ride-hailing drivers will not improve safety but will increase waiting times and benefit the taxi industry, because the requirement will limit the driver supply.

“Ninety-one per cent of the drivers on our platform drive less than 20 hours a week. These are people like single moms, students in school and people trying to supplement their incomes,” he said. “As soon as you introduce that Class 4 commercial licence , these people tend not to apply for that type of work.”

When asked if the commercial licence was a deal-breaker for Lyft, Zifkin said he was cautiously optimistic that solutions could be found working with the PTB this summer.

The Surrey Board of Trade, although pleased that ride hailing has finally received the green light in B.C., is also disappointed with the Class 4 licence requirement.

“This needs to be revisited by government to enable full market participation in the ride-hailing industry,” said Anita Huberman, CEO of Surrey Board of Trade.

The B.C. Taxi Association, meanwhile, say the Class 4 requirement shows the NDP government cares about public safety.

“I believe the government has taken the time to make sure they do not repeat the same mistakes that were made in other parts of Canada and the world,” said association president Mohan Sing Kang. “We have never said no to Uber or ride sharing … but we’ve always stated that they must meet the safety standards and there also has to be an even playing field, because they are doing the same type of job. The taxi industry will not be able to compete with them unless the rules and ground rules are identical.”

Ian Tostenson of Ridesharing Now for B.C., a coalition sponsored by Uber and Lyft, said he doesn’t expect the Class 4 requirement will kill ride hailing, but it will slow its roll out.

“What I’m worried about is if (ICBC) is staffed up, geared up and trained up to handle the onslaught of people (applying for Class 4),” he said. “I hope they’ve anticipated this because you can imagine all the road tests that would happen for Class 4 and you have to have qualified (ICBC driver) examiners — and where are you going to get those guys?”

An ICBC spokesperson said ICBC is prepared to increase the number of available Class 4 road test appointments to support additional demand.

ICBC will also introduce a new insurance policy for drivers and vehicles operating with ride-hailing companies, effective this September. The policy is a blanket, per kilometre insurance product that provides third-party liability and accident coverage.

Drivers working with ride-hailing companies would be required to have their own basic vehicle insurance policy when they are not working.

It will also be left to the PTB to decide how many ride-hailing vehicles will be allowed to operate, what boundaries if any are applicable and what rates would be charged.

“It was decided many months ago by the all-party committee to not have boundaries, to not put a limit on drivers and let the market determine pricing,” Tostenson said.

“We believe the tone coming from the Passenger Transportation Board is one of flexibility, so we don’t expect anything to be concerned about when the rules eventually do come out.”

Uber has yet to respond to the news officially, though a spokesman said the company was reviewing the details announced Monday before discussing publicly how it might impact the company’s entry into B.C.

Condo flippers beware: The taxman is watching you, and has new tools at his disposal to ‘take action’

The CRA’s ability to hunt you down over your real estate transactions is better than ever; this tax case looks at what constitutes a flip

A condo building in downtown Toronto.Jack Boland/Toronto Sun/Postmedia Network

If you plan on selling a home or condo that you bought fairly recently, especially if you never actually moved into it, be wary as the tax man will be carefully watching how you report any gain on your tax return, lest it be seen as a “flip” and be fully taxable as income, rather than a half-taxable capital gain.

The Canada Revenue Agency’s ability to hunt you down over your real estate transactions has improved thanks to the recent $50-million boost in funding over five years announced in the 2019 federal budget to help “address tax non-compliance in real estate transactions.” The CRA uses advanced risk assessment tools, analytics and third-party data to detect and “take action” whenever it finds real estate transactions where the parties have failed to pay the required taxes. Specifically, the CRA is focusing on ensuring that taxpayers report all sales of their principal residence on their tax returns, properly report any capital gain derived from a real estate sale where the principal residence tax exemption does not apply, and report money made on real estate “flipping” as 100 per cent taxable income.

But what, exactly, constitutes a real estate flip? That was the subject of a recent Tax Court of Canada decision, released this week.

The case involved a transit operator for the Toronto Transit Commission who, along with his brother, bought and moved into a two-story, three-bedroom townhouse in Vaughan, Ontario, in 1999. His brother contributed toward the initial down payment, lived with him and together they equally shared all household expenses, including the mortgage payments. In 2003, the taxpayer’s brother met the woman who would become his future wife, whom he married in April 2007. She moved into the townhouse and they had a child together in February 2008.

Sometime prior to this, the taxpayer and his brother began discussing going their separate ways. The taxpayer testified that he wanted to sell the townhouse and move to a place that was smaller and closer to work. Indeed, in 2006 he found a smaller place, a two-bedroom condo, which was in the pre-construction phase. The tentative occupancy date of the condo was April 2008, but that date was pushed back several times, ultimately to 2010.

Prior to taking possession of the condo, however, circumstances changed. In December 2008, the brothers’ father passed away while in Jamaica, where he lived together with their mother for about six months each year. Following their father’s death, their mother did not feel safe living alone in Jamaica and in March 2009 she moved into her sons’ townhouse. The taxpayer testified that his brother and his family shared the master bedroom, while the taxpayer and their mother each occupied one of the remaining two bedrooms. This living situation didn’t last long and the taxpayer refinanced the mortgage on the townhouse in order to buy out his brother’s share of the property, enabling him and his family to move out.

In August 2010, the taxpayer took possession of the condo and immediately arranged to list it for sale, realizing that it would be too small for both he and his mother. No one lived in the condo in the interim. He sold it in October 2010 resulting in a net gain of $13,412, which the taxpayer reported as a capital gain, taxable at 50 per cent, on his 2010 tax return. The CRA reassessed him, finding that the $13,412 should have been reported as fully taxable income and slapped him with gross negligence penalties.

The common question of whether a gain from the sale of real estate is on account of income or on account of capital always comes down to the underlying facts. The courts will look to the surrounding circumstances and, perhaps most importantly, the taxpayer’s intention.

The judge reviewed the facts in light of the four factors previously enumerated by the Supreme Court of Canada by which these types of cases are decided: the taxpayer’s intention, whether the taxpayer was engaged in any way in the real estate industry, the nature and use of the property sold and the extent to which the property was financed.

The taxpayer testified that he purchased the condo with the full intention of living in it after his brother moved out of their shared townhouse; however, when his father died and his mother wished to return to Canada to live full-time, the taxpayer “changed his plans to move so that his mother could live with him at (the townhouse), which was a larger space.” He testified that since he could not afford to own both homes, he listed and sold the condo shortly after assuming title. As he testified, if not for his father’s death and his mother’s return to Canada, he would have carried out his plan to sell the townhouse and live in the condo as his primary residence.

The judge concluded that the taxpayer’s intention with respect to the condo was indeed to live in it as his primary residence. He had no secondary intention of putting the condo up for resale at the time of purchase.

The judge therefore concluded that the sale of the condo was properly reported as a capital gain and ordered the CRA to reassess on that basis and cancel the gross negligence penalties.

One final note is warranted: while justice was ultimately done and the taxpayer prevailed, it actually took him nine years and three separate visits to court to get relief. The CRA originally reassessed his 2010 capital gain as income back in 2014. The taxpayer filed a Notice of Objection to oppose the reassessment, which was reconfirmed by the CRA in January 2016. The taxpayer then had 90 days to appeal the CRA’s reassessment to the Tax Court. For a variety of reasons, he missed that deadline and ended up in Tax Court seeking an extension of the deadline to file an appeal. The Tax Court denied his request for an extension. He then went to the Federal Court of Appeal which, in June 2017, reversed the lower court’s decision and allowed an extension of time to appeal to Tax Court, which heard the case in March 2019 and released its decision this week.

“While sales activity in Canada’s three westernmost provinces appears to have stopped deteriorating, it will be some time before supply and demand there becomes better balanced and the outlook for home prices improves,” said Gregory Klump, CREA’s chief economist in a press release.

“While sales activity in Canada’s three westernmost provinces appears to have stopped deteriorating, it will be some time before supply and demand there becomes better balanced and the outlook for home prices improves,” said Gregory Klump, CREA’s chief economist in a press release.