No need to tweak B-20 stress tests for ‘shrewd’ Canadians: Scotia CEO

Bank of Nova Scotia’s chief executive officer believes Canadian consumers are in good shape amid high household indebtedness and a shifting real estate landscape.

“Canadian consumers have been pretty shrewd, in terms of the choices they make, whether they go variable in the mortgage market or fixed rate in the mortgage market,” Scotia CEO Brian Porter told BNN Bloomberg in a Tuesday interview.

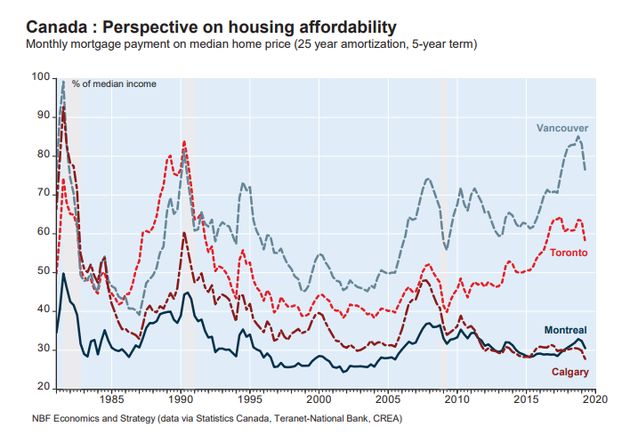

Porter added that the B-20 mortgage stress tests that took effect in 2018 have succeeded in cooling Canada’s hottest housing markets.

“B-20 and the mortgage market – in terms of the qualifying rate – has had its intended impact,” he said. “So, real estate markets in Canada – Vancouver and Toronto – are in balance and that’s a good thing.”

And while some housing industry insiders have urged the Office of the Superintendent of Financial Institutions to relax, or abandon, the B-20 mortgage stress tests, Porter said it’s best to stand pat for now.

“You have to see these through different economic cycles, too,” Porter said. “The economy in Canada is pretty good, on a relative basis, to everywhere else in the world.”

“So, I wouldn’t be doing any tweaking [to B-20] right now, but the government has the ability to do that over time.”

Scotiabank topped analyst expectations Tuesday with its fiscal third-quarter earnings. While double-digit growth in the bank’s international division fetched headlines, it was Scotia’s core Canadian banking business that led the way as profit at home rose three per cent to $1.16 billion.

“Our business here in Canada is growing very nicely, our business loans are growing nicely, credit cards – because expenditures are up – are growing very well against a somewhat slower environment here in Canada, but our business did very well,” he said.

The Canadian banks’ loan books have come under scrutiny recently, most notably by ‘The Big Short’ portfolio manager Steve Eisman, who has placed short calls on three major Canadian banks.

Porter, however, isn’t worried about credit quality at Scotia.

“We’re very comfortable with our credit trends here in Canada and outside of the country,” he said.